New look

KeithHennessey.com has a new look. I hope you like it. It’s still evolving, so expect more changes. I rushed this out the door because of the technical difficulties I had recently.

Technical difficulties

If you have tried to visit within the past 24 hours you already know that I have had some technical difficulties.

My content is now back up. I’m still tweaking some things.

I have decided to take advantage of this necessary maintenance work to put in place a new design.

I apologize for any inconvenience.

How to measure health care cost control

I want to propose a four-part test for measuring any particular bill on health care cost control.

|

short run |

long run |

|

| Federal deficit |

1 |

2 |

| Government health care spending |

X |

3 |

| Private health care spending |

X |

4 |

In each case, I will define the test so that “yes” is a good outcome:

Test 1: The bill does not increase the federal deficit in the short run.

Test 2: The bill significantly reduces the federal deficit in the long run.

Test 3: The bill significantly slows the growth of government health care spending in the long run.

Test 4: The bill significantly slows the growth of private health care spending in the long run.

I believe our Nation’s long-term fiscal problems, and the problems resulting from the growth of per capita health care spending, are higher priorities to solve than reducing the number of uninsured Americans now. I would rather solve America’s health care cost problems of the future than expand government now. This is my value choice. I expect and accept that others will disagree.

As a result of this value choice, I believe any bill that fails any one of these four tests is fiscally and economically irresponsible, and therefore worth defeating.

There does not have to be a tradeoff. A bill could go after the core policy drivers of health care cost growth, especially the tax exclusion for employer-provided health insurance, and replace it with incentives for individuals to shop for high-value health insurance and high-value health care. Such a bill could meet all of the above tests and significantly reduce the number of uninsured. I will describe such a bill in a future post. Such a bill is not going to be passed by this Congress.

I think the administration would agree with my test. They might define Test 3 to be a subset of Test 2. I think it’s important analytically to separate the two.

In practice the test gets slightly more complex. Test 1, “The bill does not increase the federal deficit in the short run,” breaks down into (1A) “over the next five years” and (1B) “over the next ten years.” The Congressional budget rules require that a bill not increase the federal deficit over the next five years. To his credit, the President and his advisors have also been emphasizing that it is important to meet the same test over the next ten years. From a formal legislative process standpoint, only the five-year window is formally binding, because Congress passed a 5-year budget plan (called a budget resolution). In particular, proponents of a bill will need 60 votes in the Senate for any bill that fails (1A). All other tests can be violated and passed with a simple majority.

I will apply this four-part test framework to each major legislative proposal considered by Congress. I want to begin today by walking briefly through each test.

Test 1: The bill does not increase the federal deficit in the short run.

I would like to make this test more stringent – my personal policy preference would be “The bill reduces the federal deficit in the short run,” especially given the path of expected budget deficits under the President’s budget. The actual test, “does not increase,” is the test in the Congressional budget resolution. It says that at a minimum, any new spending should be offset.

I would also like to make the test apply to federal spending, rather than just the federal budget deficit. I would almost certainly oppose a bill that increases government spending over the next ten years by a few hundred billion dollars, and offsets it with the same amount of tax increases. Again, I’m matching my test to the minimally binding one that Congress will apply to itself. This means that this test for me is one-way: any bill that fails it should be opposed, and some bills that pass it should still be opposed, because they dramatically increase the size of government. Still, for the purpose of this exercise I am applying the looser deficit-based short-term test.

By choosing a looser short-term test than I would prefer, I believe I accomplish two goals:

- This test conforms with the formal budget rules that will govern this bill (measured over a five year period).

- This test fits the “Blue Dog” / conservative Democrat / moderate Republican view of the world. I think I’m taking away an excuse for them to object to my four-part test.

Test 2: The bill reduces the federal deficit in the long run.

For each of these tests, I’m defining “long run” as more than ten years. That’s an arbitrary breakpoint.

While I’m willing to say I could swallow some bills that do not increase the short-term budget deficit, a bill must significantly reduce the long-run federal deficit to be fiscally responsible. Given that our long-term federal deficit path is unsustainable to the point of national economic collapse, and given that health care cost growth is one of the primary drivers of that deficit path, not making the problem worse is insufficient. A bill must result in dramatic reductions in future budget deficits to be fiscally responsible.

This test interacts with Test 3 in a somewhat subtle way. While Test 1 is a deficit test, the facts of our long-term budget problem mean that Test 2 is driven by Test 3, which is about government spending on health care.

Test 3: The bill significantly slows the growth of government health care spending in the long run.

Test 2 is about the long-term budget deficit. Test 3 is about long-term government spending on health care. The President and his budget director are correct when they identify unsustainable per capita health care spending as a primary driver of long-term deficits. (They are incorrect when they identify it as the primary driver of long-term deficits, and dismiss the importance of Social Security spending and aging of the population, as the President did yesterday. I will return to this point in a future post.)

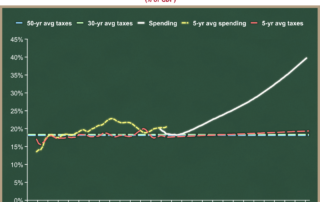

In mid-April I explained that America’s long-term budget problems are driven by unsustainable spending growth, and not by the level of taxation. I think it’s one of my most important posts. I hope you will find time to read it if you have not done so already. Here is the key graph:

On the above graph, the white line is federal spending, and the dotted lines are various tax policies. The expanding gap between the white line and the dotted lines is the federal budget deficit. You can see the gap (deficit) explodes as the spending line pulls away from the tax lines.

America’s long-term budget problems are driven entirely by the difference between the slope of the white spending line and the dotted tax lines. Over the long run, a constant tax policy always grows as fast as the economy, and so it remains flat on a graph that measures quantities as a share of the economy. So while we can and do debate about the level of the dotted tax lines, they’re always going to be flat.

You can see that any flat tax line cannot keep up with a rapidly growing upwardly sloped white spending line. Even if you were to rais the flat dotted line to 25% of GDP, you would still have a long-term deficit problem because of the slope of the spending line. The key to success is not just lowering federal spending, it’s tilting that white line dramatically downward. This is what the President and his budget director correctly mean when they say we need to bend the (government) cost curve downward. And they deserve praise for identifying federal health care spending as a major driver of that white line’s slope.

It is therefore odd and self-contradictory that they have proposed raising taxes to offset the higher spending of a new health care entitlement for the uninsured. While you can technically meet my short-term Test 1 by doing so (in a Blue Dog / centrist way that I would oppose, but you’d meet it), it is mathematically impossible in the long run to offset a new health care entitlement with higher taxes, unless your bill also slows the growth of health care spending in other ways.

To put it graphically:

- The new health care entitlement for those who are now uninsured would raise the level of the long-term white federal spending line.

- Even if you increase taxes, raising the dotted federal tax lines so that the deficit gap between spending and taxes over the next five or ten years does not increase (thus meeting my Test 1), in the long run the new health care spending will grow faster than the economy, while the new tax revenue stream will grow at the same rate as the economy. You will therefore be exacerbating the long-term deficit problem caused by the white spending line above.

- The only way to solve this is if you make other changes in the bill that bend downward the slope of the white line.

This last bullet is the President’s stated solution. In effect, he is saying, I’m OK raising long-term federal spending on a new health care entitlement, and thus raising the level of the white line in the long run, as long as we raise the dotted tax lines to offset it in the short-run, and as long as we make other changes to tilt that white line downward (or at least not upward so much.)

The President and his allies have a problem, in that their specific policy of expanding pre-paid health insurance to tens of millions of uninsured Americans will instead increase the slope of the white spending line. The academic evidence is clear that as third-party payment for health care increases, sensitivity to cost decreases and health care spending (total and governmental) increases. Creating a new entitlement for the uninsured helps the uninsured. But it worsens our long-term budget problem in two ways: it raises the level of the long-term spending line, and it increases its slope. Both exacerbate an already-devastating long-term federal budget picture.

So for the President to meet his stated goal, and to make any significant progress on our long-term budgetary problems, the rest of the bill must not only bend the spending line downward, it must do so by more than these two factors that raise the white line by creating a new health care entitlement. I think it’s a mistake to make your most serious problem worse before trying to solve it.

Test 4: The bill significantly slows the growth of private health care spending in the long run.

This is closely related to but separate from Test 3. I praise the President for correctly identifying society-wide health care cost growth as the problem to be solved, rather than just government health care cost growth or the number of uninsured. Private sector health care cost growth is what keeps the number of uninsured high, and it is what squeezes the wages and budgets of more than 200 million Americans with private health insurance. We must make policy changes that stop distorting behavior to encourage unsustainable cost growth in private sector health care.

As I said above, the expansion of third-party payment for the uninsured exacerbates this problem, as would any policy changes that might discourage people from moving to high-deductible plans, or discourage people from shopping for health insurance or medical care based on quality and price.

The President correctly identifies this problem. He admirably says it is a condition that must be met by health care legislation. Unfortunately, he has made no specific policy proposals that would achieve this goal. The President and his budget director emphasize policies that would provide private sector consumers with better information about the health care they use. They have proposed policies that would change government spending policies. They have proposed no policies that would change incentives for private consumers of health care. (I wrote about this in April.) Without such policies, you cannot meet Test 3 or Test 4. And without such policies, expanding government entitlement spending is horribly irresponsible in the long run.

The belt-and-suspenders of the Kennedy-Dodd health care bill

There is much debate about whether a health care reform bill should include a government-run health insurance plan, a so-called “public option.” Advocates argue that such a plan can compete fairly with private health insurance, and that this competition would “keep insurers honest.” They also argue that more choices are a good thing.

I fall in the other camp. I think that government cannot compete on a level playing field with the private sector. Government always has advantages because of its sovereign power. I also think that in most markets there is a range of private health insurance plans competing for business, and so the addition of one more plan is not worth the downsides of government involvement. (I believe that competition is flawed because for most people their employer shops for health plans. I prefer a system in which individuals are shopping for health plans.)

The government cannot compete on a level playing field with private firms:

- Fannie Mae and Freddie Mac had competitive advantages relative to their purely private counterparts. They leveraged those advantages to the gain of their management and shareholders until they collapsed and jeopardized the entire financial system.

- Ford Motor Company was not bailed out. It is now disadvantaged relative to GM and Chrysler, which benefited from government oversight, funding, and effective rewriting of bankruptcy rules.

- Government-provided terrorism reinsurance is preventing private reinsurance from returning to the marketplace.

- Most physician- and hospital-reimbursement structures are based on the methodologies of the largest payor in the market, Medicare.

- Government-run direct student loans are now crowding out the guaranteed student loan program, in which private banks and financing firms offer loans. The government advantage comes from control over small details of the program that give direct loans a competitive advantage.

(I would appreciate further examples if commenters have any. Updates are in green.)

The ultimate fear of having a government-run “public” option is that it will crowd out private health insurance, and that ultimately most Americans will be getting their insurance from the government.

At the same time, I hope that opponents of Kennedy-Dodd and the developing House Democrats’ health care bills don’t miss a critical point. Even if the public option is successfully stricken from this legislation, the Kennedy-Dodd goals will be largely achieved by other parts of the bill.

Separate from the Kennedy-Dodd language that creates a new public option, other language in the bill:

- Gives a government-appointed Medical Advisory Council the ability to determine a standardized package of minimum benefits;

- Establishes three tiers of standardized copayments and deductibles, as well as the total dollar value of benefits included relative to an industry average;

- Mandate relative premiums for people with different risk profiles;

- Gives the Secretary of Health and Human Services authority to set a maximum percentage of administrative expenditures and profits for health plans;

- Requires plans to provide incentives for certain models of delivery of medical care; and

- Gives State “Gateways” authority to redistribute resources among health plans to account for the risk distribution of their beneficiaries.

If the government determines benefits, cost-sharing, relative premiums, expenses, and profits, and can take funds from one health plan and give them to another, then the insurance function is governmental.

The ultimate fear of a public option would be immediately implemented by other parts of the Kennedy-Dodd bill. Health plans would turn into a version of Fannie Mae and Freddie Mac: they would have (regulated) private profits but public purposes. (A friend points out that the Fannie/Freddie comparison doesn’t work well here. F/F are more about “private profit but public risk.”)

This is a smart tactical move by the authors of the bill. They have a belt (the public option) and suspenders (government control of private insurance). They achieve their policy goal even if they lose the public option.

Killing the public option is essential, but it isn’t enough to prevent government-run health care.

Ten more things about the official Kennedy-Dodd health care bill

The Senate HELP Committee staff has filed an official copy of their draft legislation with the Senate clerk. A friend and I were discussing today two possible tactical scenarios:

- The weekend leak forced the majority staff to release their official text as damage control. Under this scenario, filing the official copy is a damage mitigation strategy: “If there’s going to be a version out there, let’s at least have it be a version we want.”

- The weekend leak was by the majority staff, and filing the official text is part of a gradual rollout strategy.

I’m guessing scenario 1 is right. Either way, we now have official text to chew on. This text is more expansive than the leaked version I posted Monday. It contains some new items, but is largely identical to the leaked draft.

More importantly, I have now had more time to read the 615 page bill. (I skimmed some parts.) Doing so turned up some things I missed the first time. So here are ten more things you should know about the official draft of the Kennedy-Dodd health care bill.

(Editorial note: I have made a page that will always have the latest version of this complete list, along with the comparison to the House Democrats’ bill. I will also post when I update that page.)

<

ol>

A few inside friends confirmed my guess – they think this is a tactical move by the majority staff to try to relieve blowback from the employer groups: Chamber of Commerce, Business Roundtable, NFIB (the small business lobby), etc. Until it is otherwise demonstrated, I will continue to assume that the Chairman’s mark will include language that will roughly parallel that in the leaked draft.

Specifically, section 2704(a) is the “Requirement to provide value for premium payments.” A health plan must report how much of their premium revenues are used for clinical services, how much for “activities that improve health care quality,” and how much for “all other non-claims costs.”Section 2704(b)(1) then tells the Secretary to look at how much other health plans spent on “all other non-claims costs,” and based on that survey, set an allowable percentage for this category. Plans are then required to rebate premiums if they go above this amount. This is direct (but confusing) regulation of premiums and profit margins.I found the labeling of this section interesting. It appears that this section will be the justification for the claim that this bill reduces health care costs. Loosely phrased, it appears their argument will be “We’re reducing health care costs by forcing plans to lower their administrative costs and profits.”

Section 3101(m) requires qualified health plans to develop and adopt a strategy “that provides increased reimbursement or other incentives for … improving health outcomes … including through the use of the medical home model defined in section 212 [of the] Affordable Health Choices Act, for treatment or services under the plan or coverage;”Section 212 then sets up the “medical home model” over seven pages of legislative text. I am far from an expert in plan-provider relationships, and am not familiar with the medical home model. But the language looks highly prescriptive, as if it is defining an extensive set of rules about the interactions among plans and different types of providers. I would love help from some commenters on what’s going on here, or some more education about the “medical home model.” My instinct is that, even if it is a good delivery model, the federal government should not be tilting the playing field for or against it.

This gives the people running Gateways a tremendous amount of power over health plans.

This looks like a fallback. Traditionally, health advocates on the Left have wanted to allow near-retirees (55-64) to “buy in early” to Medicare. And I need to be clear – I cannot conclude that this provision was written specifically to benefit the UAW VEBA. I just know that it allows a VEBA to apply as an employer for a share of this fund, and that the UAW VEBA is the most prominent one that might ask for such funds.

Remember, you can now always find an updated version of the complete list here.

While the list of two dozen items surely creates an impression of why I oppose this bill, I would like to put some structure on it. I hope to post in the next few days a higher-level view that crystallizes my biggest concerns with this bill in a structure that is easier to understand.

(photo credit: Wikipedia)

Radio: Ed Morrissey Show

Today is my debut on Blog Talk Radio. I’ll be on the Ed Morrissey Show at 3:30 PM EDT today discussing health care.

(photo credit: Radio Daze by Ian Hayhurst)

Understanding the House Democrats’ health care bill

Yesterday I posted and described the draft Kennedy-Dodd health care bill. Today I would like to do the same for an outline produced by House Democrats.

Here is a three-page outline of “Key Features of the Tri-Committee Health Reform Draft Proposal in the House of Representatives,” dated yesterday (June 8, 2009).

The three committees are:

- The House Ways & Means Committee, chaired by Rep. Charlie Rangel (D-NY). The Health Subcommittee is chaired by Rep. Pete Stark (D-CA).

- The House Energy & Commerce Committee, chaired by Rep. Henry Waxman (D-CA). The Health Subcommittee is chaired by Rep. Frank Pallone, Jr. (D-NJ).

- The House Committee on Education & Labor, chaired by Rep. George Miller (D-CA). The Health, Employment, Labor and Pensions Subcommittee is chaired by Rep. Robert Andrews (D-NJ).

The document suggests this is a joint product of the three committees and/or their subcommittees. My sense, however, is that it is Speaker Pelosi who is driving the bus. This is in contrast to the Senate, where the committee chairmen (Kennedy/Dodd and Baucus) appear to have the pen, in less well-coordinated efforts.

Kennedy-Dodd and the House bill outline are remarkably similar. Whether this represents House-Senate coordination or parallel thought processes is unclear.

I think the easiest way for me to present the House bill outline is in comparison with the Kennedy-Dodd bill. So here my description from yesterday of the Kennedy-Dodd bill, with today’s comparison to the House bill outline in red. I hope it’s comprehensible and useful this way. If you read yesterday’s post, you can skim the text in black and focus on the new text in blue.

Here are 15 things to know about the draft Kennedy-Dodd health bill and the House bill outline.

<

ol>

- All health insurance would be required to have guaranteed issue and renewal, modified community rating, no exclusions for pre-existing conditions, no lifetime or annual limits on benefits, and family policies would have to cover “children” up to age 26.The House bill outline is consistent with but less specific than the Kennedy-Dodd legislative language. The House bill outline would “prohibit insurers from excluding pre-existing conditions or engaging in other discriminatory practices.” I will keep my eye on what “other discriminatory practices” means in the legislative language. Does that mean that a health plan cannot charge higher premiums to smokers? Like the Kennedy/Dodd bill, the House bill outline would preclude health plans from imposing lifetime or annual limits on benefits: “Caps total out-of-pocket spending in all new policies to prevent bankruptcies from medical expenses.” This would raise premiums for new policies. The House bill outline “introduces administrative simplification and standardization to reduce administrative costs across all plans and providers.” I don’t know what this means, but suggest keeping an eye on it.

- A qualified plan would have to meet one of three levels of standardized cost-sharing defined by the government, “gold, silver, and bronze.” Details TBD. Same: “… by creating various levels of standardized benefits and cost-sharing arrangements…” It also contains this addition relative to Kennedy-Dodd: “… with additional benefits available in higher-cost plans.” But note the “various levels of standardized benefits.” This appears to be more expansive government control of health plan design than in the Kennedy-Dodd draft.

- Plans would be required to cover a list of preventive services approved by the Federal government.This is unspecified in the House bill outline. We’ll have to wait to see legislative language.” The House bill would require plans to “waive cost-sharing for preventive services in benefit packages.”

- A qualified plan would have to cover “essential health benefits,” as defined by a new Medical Advisory Council (MAC), appointed by the Secretary of Health and Human Services. The MAC would determine what items and services are “essential benefits.” The MAC would have to include items and services in at least the following categories: ambulatory patient services, emergency services, hospitalization, maternity and new born care, medical and surgical, mental health, prescription drugs, rehab and lab services, preventive/wellness services, pediatric services, and anything else the MAC thought appropriate.This appears parallel but is less specific for now: “Independent public/private advisory committee recommends benefit packages based on standards set in statute.” I find the “standards set in statute” interesting. It suggests that provider and disease interest groups will have two fora in which to lobby for their benefits to be mandated: Congress, and the advisory committee.

- The MAC would also define what “affordable and available coverage” is for different income levels, affecting who has to pay the tax if they don’t buy health insurance. The MAC’s rules would go into effect unless Congress passed a joint resolution (under a fast-track process) to turn them off.The House bill outline is silent on this.

- Changing (how?) the Medicare reimbursement for doctors, called the “Sustainable Growth Rate” (SGR).

- “Increasing reimbursement for primary care providers”

- “Improving” the Medicare drug program. I won’t be surprised if, when I see the specifics, I disagree that their changes are “improvements.” In the past this has meant having the federal government mandate specific prices for drugs.

- Cutting payments to Medicare Advantage plans.

- Expanding low-income subsidies for seniors and eliminating cost-sharing for all preventive services in Medicare.

The House bill outline also uses positive language to describe things that might generate budgetary savings from Medicare and/or Medicaid. The hospital readmissions point is specific. The first two points could increase or decrease federal spending, depending on the specifics.

- “Use federal health programs … to reward high quality, efficient care, and reduce disparities.”

- “Adopt innovative payment approaches and promote[s] better coordinated care in Medicare and the new public option through programs such as accountable care organizations.”

- “Attack the high rate of cost growth to generate savings for reform and fiscal sustainability, including a program in Medicare to reduce preventable hospital readmissions.”

This would have severe effects on the more than 100 million Americans who have private health insurance today:

- The government would mandate not only that you must buy health insurance, but what health insurance counts as “qualifying.”

- Health insurance premiums would rise as a result of the law, meaning lower wages.

- A government-appointed board would determine what items and services are “essential benefits” that your qualifying plan must cover.

- You would find a tremendous new disincentive to switch jobs, because your new health insurance may be subject to the new rules and would therefore be significantly more expensive.

- Those who keep themselves healthy would be subsidizing premiums for those with risky or unhealthy behaviors.

- Far more than half of all Americans would be eligible for subsidies, but we have not yet been told who would pay the bill.

- The Secretaries of Treasury and HHS would have unlimited discretion to impose new taxes on individuals and employers who do not comply with the new mandates. (The House bill outline is not specific on this point.)

- The Secretary of HHS could mandate that you provide him or her with “any such other information as [he/she] may prescribe.” (The House bill outline is not specific on this point.)

I strongly oppose the Kennedy-Dodd bill and the House Tri-Committee bill.

If this topic interests you, I highly recommend Jim Capretta’s blog Diagnosis.

(photo credit: speaker.house.gov)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Radio in Seattle and Detroit

I was a guest on the David Boze Show last night on Seattle radio, where we discussed the Kennedy-Dodd health bill.

This morning Frank Beckmann had me on his show on WJR-Detroit discussing the recent history of auto loans.

Thanks to both hosts and their producers for having me on the air.

In the future I will try to remember to provide you with advance notice.

(photo credit: Airline Tele-Dial Radio by The Rocketeer)

Understanding the Kennedy health care bill

Over the weekend a draft of Senator Kennedy’s (D-MA) health care bill leaked. After playing with Adobe Acrobat, here is the text of the draft Kennedy bill as a text file (173 K), and as a single Acrobat file (3.4 MB). Update: I fixed the broken link to the PDF. Unlike the leaked version, both of these are searchable.

Calling it the “Kennedy” bill is something of an overstatement. Senator Kennedy chairs the Senate Health, Education, Labor, and Pensions committee, and his staff wrote the draft. By all reports, however, Chairman Kennedy’s health is preventing him from being heavily involved in the drafting. Senator Reid has designated Senator Chris Dodd (D-CT) to supervise the process, but as best I can tell, it’s really the Kennedy committee staff who are making most of the key decisions. For now I will call it the Kennedy-Dodd bill.

As the committee staff emphasized to the press after the leak, this is an interim draft. I assume things will move around over the next several weeks as discussions among Senators and their staffs continue. This is therefore far from a final product, but it provides a useful insight into current thinking among some key Senate Democrats.

Update: I now have a three-page outline of the House Democrats’ health care bill. I have a new post which contains all of the content below, and compares it to the House bill. If you read the new post, you’ll get two for the price of one: Understanding the House Democrats’ Here are 15 things to know about the draft Kennedy-Dodd health bill. This would have severe effects on the more than 100 million Americans who have private health insurance today: I strongly oppose this bill. Update: If this topic interests you, I highly recommend Jim Capretta’s blog Diagnosis. (photo credit: kennedy.senate.gov)

Government Motors discussion on Fox News Sunday (continued)

In an earlier post I attempted to correct Dr. Austan Goolsbee’s incorrect and inflammatory statements about President Bush.I would like here to add my views to one additional question on the auto industry discussion on this morning’s edition of Fox News Sunday.

Host Chris Wallace moderated a discussion this morning with:

- Dr. Austan Goolsbee, Member of President Obama’s Council of Economic Advisers and chief economist on the President’s Economic Recovery Advisory Board;

- Senator Richard Shelby (R-AL), ranking Republican on the Senate Banking Committee;

- Thayer Capital Chairman Fred Malek; and

- Google CEO Eric Schmidt.

I offer kudos to Mr. Schmidt for his thoughtful responses throughout. And the hero of the discussion was Mr. Wallace, who in his questions demonstrated a deep understanding of the actual options faced by policymakers, the choices they made, and the serious consequences of those choices. I thank him for trying to elevate the policy discussion this morning.

Here’s Chris Wallace asking Fred Malek whether the Bush Administration have provided loans before a Chapter 11 filing:

WALLACE: Let me bring in Fred Malek, though. The President says that he has no interest in running businesses, he’s just trying to save them from collapse and get out.

[plays clip of President Obama’s press conference] Fred Malek, in the middle of a financial crisis, in the middle of a terrible recession, could the President really let General Motors and Chrysler, AIG and Citibank go under?MALEK: … I think what you have here, is you have two different situations. I would label the injection of capital into the financial institutions, stabilizing the financial systems, that’s a war of necessity. You had to do that. But, getting into General Motors, saving General Motors and then taking them into bankruptcy, that’s a war of choice, it’s the wrong choice.

Senator Shelby later commented on this same question, as did Mr. Malek again:

SHELBY: First of all, I advocated last fall that General Motors and Chrysler’s best bet would have go to Chapter 11 then, it would have saved a lot of money, not a political restructuring like what’s happened, where the bondholders have been sacrificed, the unions have carried the day.

MALEK: I agree with Senator Shelby. Look, we’ve had for decades we’ve had a bankruptcy system in this country that has worked well, and has fueled the free enterprise system in a positive way. It is impervious to politics because it’s run by federal courts. Now, what have you done? You have taken it out of the judicial and you’ve turned it over to the executive, and I think you’ve injected politics into it. Senator Shelby is right, there was no sense in putting billions of dollars in and then declaring Chapter 11 afterwards. They should have let them go into bankruptcy and let the courts work it through. …

Mr. Wallace then asks the critical follow-up question:

WALLACE: Let me just ask. Mr. Goolsbee, if at some point, either the Bush Administration back in the fall, or you guys when you took over, had just said, go into Chapter 11, we’re not going to take an ownership stake, we’re not going to give you 50 billion dollars, what would have happened?

The answer is that GM and Chrysler would have liquidated. Neither GM nor Chrysler was ready for a complex Chapter 11 filing. Had the entered the Chapter 11 process in December or January, the firms and every outside expert told us that the restructuring would have failed and the firms would have liquidated. We estimated this would have resulted in about 1.1 million lost jobs.

Mr. Malek was right, the loans to GM and Chrysler were a choice, but they were not the choice that he and Senator Shelby thought we faced. The choice was loan or liquidate. There was no feasible Chapter 11 option available at the time. (GM may fail even now, after they have had five months to prepare for Chapter 11.) Mr. Schmidt frames it correctly:

Schmidt: It seems to me that what choice did we have except try to save General Motors, given the roughly million jobs that were related at a time of incredible pain and job loss. So if you think about it , the choice was bankruptcy, the supply chain goes away, the loss of the American automobile industry, or a band-aid. It needs to be a band-aid, and it needs to be something we get out of.