Responding to Chrysler comments

As a novice blogger I have been repeatedly surprised and humbled by the thoughtful comments posted on this blog. I want to thank all of you who are contributing to a civil and thoughtful discussion.

At the risk of offending some of you, I am going to push back on some of the comments to yesterday’s Chrysler post, in the way that I would have done so had you been advisors to President Bush and I been in my old job at the White House National Economic Council. I’m putting my “honest broker” hat on, and I want to stress that this pushback is independent of my own policy views.

In yesterday’s post I listed five options. Option A was to withhold all additional taxpayer funds. This is the pure free market option, and also the most popular option among the commenters. I asked you to assume that choosing Option A would mean a 99% chance that Chrysler would liquidate by July 1st, and an additional 10-20% chance that GM would liquidate.

The first two commenters seem to have internalized that and be willing to bear these costs. FogCity wrote “Liquidation of Chrysler sets the stage for renegotiations with the UAW

Some of the commenters, however, want to have it both ways: choose Option A, but assume that Chrysler will not fail. I strongly support your choice of option A, as long as you accept that this choice means a few hundred thousand people will lose their jobs in the next 2-3 months, and that you will be (unfairly) blamed in public for their job loss. If you choose A, you need to assume that there will not be another buyer for Chrysler, and that the Chapter 11 process will quickly turn to liquidation, with the subsequent job loss. You’re not making a real choice if you assume that A might lead to a happy ending for Chrysler employees.

At the risk of overemphasis, I want to make it clear that I think there is a very strong case you can make for Option A, and several of the commenters are making it. But that case has to be structured as “I’m for option A because _________, even though several hundred thousand people will lose their jobs. The long-term benefits of option A are worth the short-term costs to Chrysler workers and retirees, and to the Upper Midwest region.” To refine the political side of it, ask yourself if you would be willing to defend your view on a Detroit TV station or in an interview with the Detroit Free Press.

I hope that this response will be interpreted the way it is intended: as my attempt to push you to think hard about your choices, and to force you to acknowledge that there is a real tradeoff between short-term pain for hundreds of thousands of people and the long-term benefits of allowing free markets to operate unfettered. If you are for Option A, I hope you will try to make the case that these costs are worth the benefits, rather than pretending that the costs don’t exist.

Mixed results on the Chrysler announcement

The President’s Chrysler announcement last Thursday produced mixed results.

The agreement among Chrysler, Fiat, UAW, the Administration, and the large banks appears to increase the probability (from almost zero) that Chrysler will survive for the long run, albeit as a part of Fiat. This is clearly a good thing.Is it worth the cost to taxpayers and the broader damage caused by government interference in the economy?

Taxpayers will sustain Chrysler during its restructuring. (Fiat is putting up no cash.)The Administration has committed $8.1 billion of new taxpayer funding for a bankruptcy process that they think will take 60 days, followed by a transition period of unknown duration. I think the final cost will exceed this additional $8 B, in part because I doubt the 60-day timeframe. Since the Administration agreed to forgive about $4 B the taxpayer has already loaned to Chrysler, I am also pessimistic about the taxpayer’s chances of getting back this new $8+ B outlay of funds.

It appears the Administration reached agreement first with UAW and the big bank creditors, and then tried to “jam” the dissident creditors with a tough and possibly unfair take-it-or-leave-it offer. When those creditors rejected the Administration’s offer, the President publicly excoriated them.

The result may be a firm that survives, but there are serious adverse consequences of this process and dangerous precedents for the broader economy:

- Industrial policy—

- Leveraging TARP banks – It appears the Obama team pressured TARP-recipient big banks to forgive much of their loans to Chrysler. If so, they have taken a huge step toward making these banks instruments of public policy rather than private firms. This is a primary fear of “managed capitalism” – political leaders start leveraging one sector to influence another.

- Bypassing the capital structure and bankruptcy process – There is no such thing as a level playing field when the government negotiates with private parties. The Obama team set themselves up as both the arbiter of the negotiation and a participant in it. It now appears that they are trying an end-run around the Chapter 11 process through a section 363 sale. If they are successful, they will have interfered with the rights of others who thought they could rely on the traditional bankruptcy structure to protect their interests. The Obama team is introducing significant political risk into future business loans by undermining the traditional bankruptcy process. This makes future loans more expensive for firms.

- Leveraging Fiat to meet new and arbitrary fuel efficiency goals – The fuel efficiency goals mandated by CAFE come from legislative bargaining. The new targets for Fiat (e.g., a 40 mpg vehicle made in the US) were created from thin air by the Obama negotiators. Suppose they had said Fiat cannot make blue cars. Would that be OK? When combined with the apparent cross-sector leveraging of TARP banks, this suggests a scary level of micromanagement and political interference.

- The deal appears to favor the President’s political allies — UAW is part of the deal, “investment firms and hedge funds” are not. The fuel efficiency crowd is presumably happy with the new requirements imposed on Fiat. The appearance the Administration has created, reinforced by the President’s public bashing of the dissident creditors, is that they used carrots with their friends, threatened the big banks with a stick, and then hit the dissident creditors with that stick when they refused the Administration’s offer. If the reality reflects this appearance, then the Administration has abused its power in structuring the proposed deal.

- Demagoguery — The President attacked people for asking to be paid back the money they loaned. These “investment firms and hedge funds” have a legal right and a responsibility to the people whose money they invested.

It is easy to criticize the Administration’s approach and say what they should not have done. It is harder (and more responsible) to say what you would have done instead, and to accept responsibility for the downsides of that choice. If you disagree with what the President did, I challenge you to recommend an alternate path. I will give you five options. To make it hard, please assume the probabilities listed:

- Withhold all additional taxpayer funds. (99% chance Chrysler liquidates by July 1)

- Tell the negotiating team to set a goal (a viable firm without permanent taxpayer subsidies) and a limit on taxpayer funds, and then stay out of the negotiations among private parties. (70% chance Chrysler liquidates by January 1 because the Chapter 11 process drags on and Chrysler’s sales plummet)

- Do what the Obama team did, but don’t use the section 363 process to jam creditors and don’t publicly bash those creditors when they dissented. (50% chance Chrysler liquidates by January 1)

- Tell the negotiating team to lead /”help” the negotiations, but strictly instruct them not to pursue non-taxpayer goals (like fuel efficiency), and not to favor UAW over creditors. Use the section 363 process if necessary to jam an objecting party, but don’t publicly bash them. (30% chance Chrysler liquidates by January 1)

- Do what the Obama team did, and be willing to add more funds if necessary to keep Chrysler alive. (15% chance Chrysler liquidates by January 1)

Also, please assume that a Chrysler liquidation increases the chance of a GM liquidation by 10-20% through a chain reaction of parts suppliers failing.

These probabilities are my somewhat-wild guesses. If you find yourself arguing with me in the comments about the probabilities, you are missing the point of the exercise. Please assume these probabilities (even if you disagree with them) and tell us what you would do, not just what you would not do.

I will start the bidding by choosing (B).

Intro to TARP — Summary of the series

Here are the four Intro to TARP posts:

The Chrysler bankruptcy sale

Last Thursday the President announced a deal among Chrysler, Fiat, the UAW, the U.S. government, and several of Chrysler’s largest creditors. Some creditors oppose the deal, and Chrysler entered a bankruptcy process that will attempt to resolve this dispute.

The creditors left out of the deal are arguing that the Administration offered better deals to more junior creditors (such as UAW retirees) than to them. These objecting creditors think they can get a better deal from a bankruptcy judge than they were offered by the Administration.

This is not a traditional bankruptcy filing under Chapter 11. Instead, Chrysler, supported by the Administration, is using a section of the bankruptcy code (section 363) to try to sell portions of Chrysler to a new company (called “NewCo”) and dump some of the liabilities. If approved by the bankruptcy court, this would appear to give Chrysler the ability to “roll” the recalcitrant creditors and implement the deal negotiated with the other parties. The Administration appears to think this section 363 process gives them more leverage over the objecting creditors. The President has some smart and experienced people working on this, so I have no reason to doubt their judgment on this point.

Intro to TARP — TARP III: The Geithner Plan

We have so far:

- created our example of Large Bank;

- described TARP I, in which the government would buy bad assets from banks; and

- described TARP II, in which the government made direct equity investments in banks.

The Bush Administration implemented TARP II as the $250 B Capital Purchase Program (CPP), although less than $250 B has been allocated to specific banks.

Today I would like to describe TARP III, the Geithner plan now being implemented by the Obama Administration. I should warn you that this is more complex than TARP I and TARP II.

Here is the summary:

TARP III = (TARP II + stress tests + more capital targeted at big sick banks) + ( TARP I with private sector participation and more money through the Fed & FDIC)

Let us begin with the Obama Administration’s expansion of TARP II. They have:

- Left the Capital Purchase Program in place.

- Stress tested the 19 banks that have more than $100 B. Based on those stress tests, regulators will require some of these big banks to raise more capital.

- These banks “will be given a six month period to raise any additional capital needed to establish [a] buffer from private sources.” If the bank cannot raise this capital privately, then Treasury will provide it from the TARP.

The Administration calls (2) + (3) their Capital Assistance Program. It is an expansion of the Capital Purchase Program, targeted at filling the capital holes of big sick banks that cannot or will not raise funds from private investors.

Now let us turn to the Administration’s new plan to address the downside risk that Large Bank has on its balance sheet, what they call their Public-Private Investment Program.

It comes in two parts, one to help Large Bank sell its loans with downside risks, and the other to help it sell those securities with downside risks.

I will start with the Legacy Loan program, which is a little easier.

Large Bank shows their 120 of bad loans to the FDIC. The FDIC evaluates those loans and sets a ratio and a price. The ratio can be as high as 6:1. Let’s assume for these loans that the FDIC will go up to 5:1. I will describe the price in a moment.

Let’s also say that your friend Fred runs Fred’s Hedge Fund.

- Fred puts up 10 of investment capital.

- Treasury matches Fred with 10 of capital from the TARP.

- FDIC uses its 5:1 ratio to match the 20 of capital with 100 of guaranteed debt. Technically, FDIC only puts up the guarantee, while the actual funds come from other private lenders.

- Fred now has 120 (his 10 of capital + 10 from Treasury + 100 of FDIC guaranteed debt). He uses this to buy the 120 of bad loans from Large Bank.

Fred is in a great position. If these loans are actually worth 180, then he makes 60 of profit which he splits 50/50 with Treasury. He invested 10 and made 30 in profit. Not bad.

If these loans are actually worth 60, then he loses his 10 of investment. Treasury loses 10, and FDIC covers the other 40 of losses.

I said earlier that the FDIC sets a ratio and a price. The price is the amount FDIC will charge for the guarantee. This is a key variable to watch. If FDIC charges an actuarially fair price for their guarantee, then that will eat heavily into Fred’s profit. I presume that FDIC will charge less than an actuarially fair price to encourage buyers to purchase these bad loans. By lowering the guarantee price below that which is actuarially fair, the Administration and FDIC Chairman Sheila Bair have a dial they can turn to encourage buyers of bad loans and drive up the prices paid to banks for those loans.

Assuming that the guarantee price is inexpensive, this would be a great deal for Fred’s hedge fund if he had it all to himself. His upside risk is much greater than his downside risk. In fact, he would be willing to pay more than 120 for these loans that Large Bank has been valuing at 120. Other investors will recognize this opportunity and compete with Fred to buy these bad loans from Large Bank. We would expect Fred and other investors to compete away the “rent” by bidding up the price of these bad loans until they are receiving a competitive return.

The Administration looks to be throwing this process wide open, to encourage lots of buyers. The winners will be the banks with the bad loans. By subsidizing the private purchasers with debt guaranteed by the FDIC for a cheap guarantee fee, the Administration can encourage private bidders to bid up the price of these bad loans until they expect to receive a return commensurate with the risk they are taking. Since FDIC bears much of the downside risk, the price should rise.

The Administration emphasizes that private bidders will be establishing the price paid for these bad loans. This program appears to be a clever way to “overpay” the banks more than current market prices for these loans, while being able to politically say that prices were set by market forces rather than the government. They can leverage private capital and especially FDIC’s balance sheet to buy more legacy loans than if they had used TARP funds alone, and they can recapitalize banks at the same time by setting up a mechanism that should bid up the sales price for these “legacy loans.” Given that for the loan program, you have up to 11 government dollars for each dollar of private capital, I think they are overselling the private sector involvement. I think they think it helps them with their optical challenges.

The legacy securities program is similar but not identical. It works through the Federal Reserve. It is not open to as wide a range of purchasers, so some of the benefits should (I think) go to the buyers, rather than having all the rents accrue to the sellers.And it works through leveraging a separate program, called the TALF, rather than through the FDIC’s guaranteed loans. I don’t think that walking through all the mechanics of the securities program adds a tremendous amount of value, because I want to get to the conclusions.

Results (if it works):

- They fill capital holes in a broad array of banks through the Capital Purchase Program (aka TARP II).

- They supplement CPP by finding and filling capital holes in the sickest big banks through the stress tests plus targeted capital investments, aka the Capital Assistance Program.

- They buy bad assets from Large Bank and others, leveraging FDIC (for loans) and Fed (for securities) balance sheets, plus a little private money, to make TARP dollars go farther and buy more bad assets. This is good because it helps them solve more of the downside risk problem, but bad because they are exposing taxpayer to more risk.

- By subsidizing the guarantee fee and taking a lot of the downside risk, purchase prices (at least for loans) should allow banks to get more than current market prices for those assets (at least for the loans). This helps those banks dump their bad risks on the government and gives them a bit more capital.

- The FDIC and Fed bear the downside risk associated with these bad loans and securities. Ultimately the taxpayer bears the downside risk carried by the Fed. It is unclear who bears the downside risk carried by FDIC — the taxpayer or the banking industry. FDIC is supposed to be self-financing through fees on insured institutions.

- The Administration has political cover if and when market prices for these assets are above current market prices.They will continue to hide behind “the private sector choosing the prices,” even though they have distorted those prices through subsidized loan guarantees.

With TARP III the Obama Team has figured out a way to make TARP dollars go farther. They are using this extra room to try to address both the banks’ capital holes and the downside risk / bad assets problems. I hope it works.

Tactical consequences of the Specter switch

I spent more than seven years working in the Senate, including 5 and a half working for Senator Trent Lott (R-MS), in his time both as Majority Leader and as Minority Leader resulting from Sen. Jeffords’ party switch.

There is a lot of hype about how Sen. Specter’s switch from Republican to Democrat will give Senate Majority Leader Reid 60 votes, assuming that Mr. Al Franken is sworn in as a Democrat Senator from Minneota. Some are suggesting that there will be no legislative check on Democrat majorities, now that Senator Reid has 60 votes to invoke cloture and shut off filibusters.

This is an exaggeration. While Leader Reid’s tactical position is clearly stronger, given that Sen. Specter was a frequent Reid target for that 60th vote, it is important not to overstate the change.

Here are what I think will be some practical consequences of the party switch:

- I imagine Sen. Specter’s voting patterns on issues that are clearly high personal priorities for him, like judicial issues, health, and appropriations, will show almost no appreciable change. I think the same will be true for headline issues like Iraq, Afghanistan, and terrorist surveillance.

- The biggest effect will be on the small votes, as well as votes on things that are not high priorities for Sen. Specter. If he behaves like other party switchers, his new party will get many of these votes, because his default vote will switch from R to D. This benefits Leader Reid in that he has more flexibility with other Democrats who might be tempted to vote against the party on a particular issue.

- The same will be true for many procedural votes, on which I expect him to vote with his new party.

- But on cloture votes, where Sen. Specter has often been the marginal Republican vote, it is easy to imagine him being a less-than-reliable Democrat vote for cloture, just as he was a less-than-reliable Republican vote against cloture.

- Assuming Sen. Specter wins re-election, the ratio of Democrats to Republicans on committees will improve slightly for Democrats. This has a significant practical effect on the legislation that actually reaches the Senate floor.

- I assume Sen. Specter’s chance for re-election increases substantially.

The Specter switch contributes to significant short-term Democrat political momentum. The long-term legislative effect matters, but it is not as large as some observers are suggesting.

Intro to TARP — TARP II: Direct investment

Tuesday I began with a simple example, which I am calling Large Bank.

Yesterday we looked at TARP I, in which the government would buy troubled/toxic assets from banks.

Today I will describe TARP II, the plan we (the Bush Administration) implemented, in which the government made direct equity investments in banks to help fill their capital holes. We called this the Capital Purchase Program.

As a reminder,we are trying to address two problems:

- Large Bank does not have enough capital.

- Large Bank has downside risk on its balance sheet due to the uncertain value of these bad loans. That downside risk makes the firm’s value uncertain and scares away investors.

Here is the balance sheet for Large Bank:

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 120 | Debt | 300 | |

| Equity | 20 | |||

| Preferred | 0 | |||

| Total | 920 | . . . . . . . | Total | 920 |

- Total capital: 20

- Leverage: 46:1

TARP I solves problem #2 if you buy all the bad loans, but it is extremely inefficient in addressing problem #1, the capital hole. Spending 120 from the TARP to buy the bad loans would provide no new equity capital. Spending 150 to buy the loans valued at 120 would provide a net 30 of capital for 150 outlayed from the TARP.

The constraint is not the ultimate cost to the taxpayer. It is instead the legislated limit on how much outstanding cash can be invested/spent at any one time from TARP: $700 B.

To fill the capital hole, our first choice would be for the bank to attract private capital. Bank management appears reluctant to do this, because they don’t want to dilute the value of their existing shareholders. In addition, private investors were unwilling (at least last Fall) to invest in banks that had significant downside risk on their balance sheets. So temporary public capital, provided by the taxpayers, was the only option to recapitalize the banking system.

If we take the same 120 from the first TARP I case, but instead use it to buy preferred stock in Large Bank, we end up with this:

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 120 | Debt | 300 | |

| Cash | 120 | Equity | 20 | |

| Preferred | 120 | |||

| Total | 1,040 | Total | 1,040 | |

- Total capital: 140

- Capital added by this transaction: 120

- Leverage: 7.4:1

- Risk of bad loans: still lies entirely with Large Bank

- Taxpayer outlay from TARP: 120

- Long-term cost to taxpayer: Zero if the firm remains solvent, up to 120 if the firm goes bankrupt.

Results:

- Large Bank has 120 more capital from the government. It is now well capitalized and has a good leverage ratio. (I am for now glossing over the difference between preferred and common stock.)

- Large Bank still has all the downside risk associated with the bad loans. This may continue to scare away private capital, depending on estimates of the relative size of the strengthened capital cushion and the downside risk of those bad loans.

- The government has spent 120 of the TARP pool.

- The taxpayer will get dividends from the preferred stock (which look a lot like interest payments at a fixed interest rate).

- The government is now the majority investor in Large Bank and has both an ongoing taxpayer interest in and leverage over how the bank is run.

TARP II gets tremendous bang for each TARP buck in recapitalizing banks. If you are more worried about the capital hole than the downside risk, then TARP II has far better arithmetic.

If you are worried that the capital problem being bigger than you think, then you want to use TARP resources in the most efficient way possible. Remember that you do not have good information about the size of either the capital hole or the downside risk. You know what the banks report about their balance sheet, but especially last fall, we had to be extremely skeptical about the information being reported about the size of both problems. This is one reason why the stress tests are so valuable — regulators and policymakers presumably have much better information now about the absolute and relative sizes of each problem, at least for the 19 largest banks.

Over the past few months we have been experiencing a significant policy downside of direct equity investment, and it is a major difference between TARP I and TARP II. Under TARP I, the government buys the asset and the relationship between the government and the bank ends. Under TARP II, the government has an ongoing relationship with the bank. This creates policy tension among three different governmental roles:

- government as rule-setter and regulator;

- government as investor on behalf of the taxpayer; and

- government as an interested party with other policy (or non-policy) goals.

This tension is playing out in several uncomfortable and unpleasant ways. The government is involved in compensation decisions within the firm. The government is leveraging its investment to pursue other goals, like encouraging the banks to lend and maybe leveraging some of them to write down auto manufacturers’ debt. And the government may trade off other policy goals against the taxpayer’s investment by allowing banks to convert preferred equity to common equity.

Returning to the original two goals, you can see the two extremes in TARP I and TARP II. TARP I was focused on removing downside risk from balance sheets. The danger with TARP I is you might buy $700 B of bad assets, and have only made a medium-sized dent in the downside risk problem, while doing far less to fill the capital holes. TARP II ignores the downside risk problem while getting a huge bang in filling capital holes. TARP II also has other problems derived from the ongoing linkage between Uncle Sam and the banks.

Tomorrow I will describe TARP III, the Geithner approach, and how it tries to address both problems by tapping into non-TARP resources.

As in the rest of this series, I thank Donald Marron for his examples and assistance.

Intro to TARP — TARP I: Buying bad assets

Yesterday we created a simple example of Large Bank, which made some bad loans and now has two problems:

- It doesn’t have enough capital.

- It has downside risk on its balance sheet due to the uncertain value of these bad loans. That downside risk makes the firm’s value uncertain and scares away investors.

Today we examine “TARP I,” the first plan for how to address these problems.

(One commenter pointed out some oversimplifications in my example. I will continue to oversimplify. These are imperfect teaching tools designed to illustrate the conceptual differences among TARP I, II, and III.)

I am again indebted to Donald Marron for his examples and help.

As a reminder, here is the balance sheet for Large Bank:

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 120 | Debt | 300 | |

| Equity | 20 | |||

| Preferred | 0 | |||

| Total | 920 | . . . . . . . | Total | 920 |

- Total capital: 20

- Leverage: 46:1

Congress has now passed and the President has signed the TARP law. The Treasury Secretary (and, practically speaking, Federal Reserve Chairman, and FRBNY President) have a big pot of money to help Large Bank and others.

Suppose the government bought those bad loans from Large Bank for the same value that Large Bank was carrying for them:120. The balance sheet of Large Bank would now look like this:

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 0 | Debt | 300 | |

| Cash | 120 | Equity | 20 | |

| Preferred | 0 | |||

| Total | 920 | . . . . . . . | Total | 920 |

- Total capital: 20

- Capital added by this transaction: 0

- Leverage: 46:1 (Caveat: This depends on whether “cash” is actually cash or something safe like Treasuries. In practice, real leverage ratios are risk-weighted. Even if we only count the loans it is 40:1, which is still very high.)

- Risk of bad loans: cleared from Large Bank

- Taxpayer outlay from TARP: 120

- Cost to taxpayer: Whatever the losses are on the bad loans.

This is just a swap on the asset side of the balance sheet. Large Bank traded 120 of bad loans for 120 of cash from Treasury.The results are:

- Large Bank’s capital problem is unaffected. It still has only 20 of capital, and still has a very high leverage ratio.

- The downside risk associated with the bad loans has been eliminated from Large Bank’s balance sheet. This should presumably make it easier for Large Bank to attract private capital.

- The government has spent 120 of the TARP pool.

- The taxpayer now bears the downside risk associated with bad loans for which it paid 120. The expected cost to the taxpayer is less than 120. This is an investment, and we are buying something of (uncertain) value.

Now let’s look at an important variant of this plan. Suppose we do the same thing, but the government pays 150 for the bad loans which the bank had been valuing at 120. Large Bank’s balance sheet would now look like this:

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 0 | Debt | 300 | |

| Cash | 150 | Equity | 50 | |

| Preferred | 0 | |||

| Total | 950 | . . . . . . . | Total | 950 |

- Total capital: 50

- Capital added by this transaction: 30

- Leverage: 16:1 (with the same caveat as above)

- Risk of bad loans: cleared from Large Bank

- Taxpayer outlay from TARP: 150

- Long-term cost to taxpayer: Whatever the losses are on the bad loans

The bank trades 120 of bad loans for 150 of cash from Treasury. The results are:

- Large Bank has 30 more capital from the government. It now has a more reasonable leverage ratio.

- The downside risk associated with the bad loans has been eliminated from Large Bank’s balance sheet. This should presumably make it easier for Large Bank to attract private capital.

- The government has spent 150 of the TARP pool.

- The taxpayer now bears the downside risk associated with bad loans for which it paid 120.

- Elected officials and the press scream about the government “overpaying” for these bad loans and shafting the taxpayer.

We are now addressing both problems: Large Bank’s capital hole, and the downside risk of the bad assets. The downsides are that we are consuming more of our TARP pot to do so, and we have an optical problem in that we are paying banks more for these bad assets than the bank thought they were worth. Large Bank will also report a profit of 30 from this transaction, further compounding the optical challenge.

The logic of “overpaying” for bad assets becomes a little easier if we instead imagine that these are mortgage-backed securities (MBS) rather than loans. If the bank had to value these bad securities at their market value, you could end up with the following scenario:

- The bank thinks that if it held these mortgage-backed securities for the long run, the underlying mortgages would pay out and they would collect 160. This is the bank’s estimate of the “hold-to-maturity price.”

- But since the market is so nervous about the downside risk, the current market price is 120.

If the government pays 150 for these securities, is it overpaying for them? If the bank is right (or the government analysts who say they are willing to value it at 150), then the taxpayer can buy it at 150, hold it for a long time until the mortgages mature, and make 10 in profit. We would be taking advantage of the fact that the government is willing to be far more patient than private investors, and therefore willing to buy and hold these securities.

This was the argument that Secretary Paulson and Chairman Bernanke made in September of last year when they were testifying before Congress on the need for TARP legislation.

TARP I as originally conceived, buying bad assets from banks and paying prices that would partially recapitalize those banks, was aimed at addressing both problems of Large Bank. It runs into the problem of using TARP funds inefficiently. In the first example, we spent 120 from the TARP and created no new capital for Large Bank. In the second example, we spent 150 from the TARP and only created 30 of new capital for Large Bank. To the extent you are concerned with problem #1 (the capital hole), you would like to use TARP funds more efficiently. That is the principal reason we pivoted away from buying these assets (at whatever price) and toward direct equity investing in banks. Remember, that in making these choices, you don’t know how big either problem really is.

As a more general matter, the three different TARP approaches can be understood as different answers to two questions:

- What is the relative importance of filling the banks’ capital holes versus removing the downside risk from banks’ balance sheets?

- How can we use a large but limited pool of TARP funds most efficiently?

Tomorrow I will explain TARP II: Direct equity investment in banks.

Intro to TARP: Banks have two problems

The big banks (and some large non-banks like AIG, Fannie Mae, and Freddie Mac) have two problems, not one:

- They don’t have enough capital.

- They have on their balance sheet downside risk that is creating uncertainty about how much the firm is worth and is scaring away investors.

I will use a simple example constructed by former Council of Economic Advisers member Donald Marron.

Imagine that you run Large Bank. You collect deposits and you borrow on the debt market, and you use both sources of funds to make loans. Here is what your balance sheet looked like three years ago when you made these loans.

| Assets | Liabilities and Equity | |||

| Loans | 1,000 | Deposits | 600 | |

| Debt | 300 | |||

| Equity | 100 | |||

| Preferred | 0 | |||

| Total | 1,000 | . . . . . . . | Total | 1,000 |

To keep it simple, let us assume that all 1,000 of loans were for home mortgages.

We measure the health of your bank in three ways:

- You have 100 of capital — the equity from the shareholders who invested in your bank.

- Your leverage ratio is 10 to 1 — you are supporting 1,000 of loans with 100 of capital.

- Can you roll over your debt and issue new debt when you need/want to? Do creditors have enough confidence in your bank that they are willing to loan you money?

A healthy bank is one with a lot of capital, with a leverage ratio that is not too high, and that can borrow when it needs to at reasonable interest rates. Of course, the higher the leverage ratio, the more profit you make on each dollar of capital.

Now let us assume that you screwed up three years ago. 200 of the 1,000 of loans you made were “no documentation” loans.Some (many? most?) of those 200 of loans are going to default, or at least be late with some of their payments. They are clearly not worth the 200 of face value. First let’s separate out the good and bad loans.

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 200 | Debt | 300 | |

| Equity | 100 | |||

| Preferred | 0 | |||

| Total | 1,000 | . . . . . . . | Total | 1,000 |

Now in present day, you estimate that 80% of those bad loans will default, with a 50% recovery rate, so they are worth only 120 (60% of 200). You write down the value of the bad loans to 120, losing 80 on the assets side. This means the value of your equity has dropped from 100 to 20.

| Assets | Liabilities and Equity | |||

| Good loans | 800 | Deposits | 600 | |

| Bad loans | 120 | Debt | 300 | |

| Equity | 20 | |||

| Preferred | 0 | |||

| Total | 920 | . . . . . . . | Total | 920 |

Writing down these loans has wiped out 80% of your capital. Problem #1 is that you only have 20 left of capital. This also leaves you with a very high leverage ratio of 46:1 (920 of loans divided by 20 of capital). Large Bank is clearly not in good shape.Creditors will start charging you higher interest rates for new debt (or to roll over existing debt), and any uninsured depositors may get nervous and pull their money out.

If you can raise more capital by selling more equity, you can give yourself more protection against insolvency and reduce your leverage ratio. Your existing shareholders will be upset, because before they owned 100% of the profits, and after raising more capital they will own a much smaller share. If you raise new private capital, you will be “diluting” your existing shareholders. This is one possible explanation why some banks have not raised capital so far.

You have a second problem, however. As you try to raise more capital and sell equity to new private investors, they are questioning the value of those bad loans. Sure they might be worth 120, but they might be worth only 100, or 80, or even 60.A private investor thinking of putting 60 of his own capital into Large Bank could see that get wiped out if the bad loans are only worth 40 rather than 120. The downside risk associated with those bad loans may deter private investors from putting in their own capital.

So Large Bank has two problems. You don’t have enough capital, either to satisfy your regulator or to reassure yourself that you won’t soon go insolvent if things get even worse.

You also have downside risk which makes the health of your bank even shakier than the above balance sheet suggests, and which scares away private investors.

Tomorrow we will look at three different ways to address your problems, aka TARP I, II, and III.

{kind=link}

Sloppy energy language: dependence on foreign oil

This is good language from the President in bold:

America’s dependence on oil is one of the most serious threats that our nation has faced.

This is not:

They’ll be jobs building the wind turbines and solar panels and fuel-efficient cars that will lower our dependence on foreign oil …

Nor is this:

And just last week I visited the Electric Vehicle Technical Center in Pomona, California, which is testing batteries to power a new generation of plug-in hybrids that will help end our dependence on foreign oil.

Is the U.S. dependent particularly on foreign oil, or just to oil? Is there anything we can do to break our “addiction to” or “dependence on” foreign oil?

In the Bush White House, policy staff worked hard over several years to excise the phrases “dependence on foreign oil” and “addiction to foreign oil” from the President’s prepared remarks. I hope the Obama team goes through the same effort. Sloppy language on this point creates expectations that can never be met by policy.

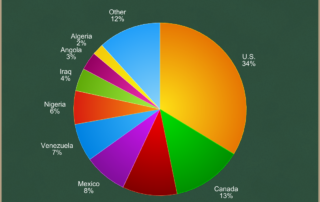

In 2008 the U.S. consumed an average of 14.7 million barrels of crude oil per day. U.S. suppliers produced just under 5 million barrels per day (bpd), meaning we imported 9.8 million bpd from the rest of the world.

You might be surprised to know that two of our top three foreign suppliers are Canada and Mexico. Here is where U.S.-consumed oil came from in 2008:

Well, that’s easy, you might say. Domestic production is fine, and Canada and Mexico are friendly and stable neighbors. How much oil do we get from unstable or unfriendly parts of the world? Maybe 30-40%? So if we reduce our oil demand by 40%, then we don’t need to import oil from the Middle East, or Venezuela or Nigeria. Problem solved. We will have eliminated our dependence on foreign oil, or at least on foreign oil from unstable or unfriendly parts of the world. (I will ignore for the moment whether it is feasible to reduce domestic oil demand by 40%.)

This is the flawed logic that supports the phrase “dependence on foreign oil.” It suggests that we can control the source of American oil. We cannot, and even if we could, it would not matter.

Two things matter to U.S. citizens when we think about imported oil:

- Large portions of the global oil supply are vulnerable to shocks. These shocks, hurt all consumers of oil, no matter where they occur.

- A significant share of U.S. income goes to people we do not like (e.g., President Chavez’ government) to pay for the oil they supply us. They use these profits to do things we do not like.

Imagine a huge reservoir, being filled by a handful of large rivers and a whole bunch of tiny streams. Several of the large rivers are controlled by governments (labeled “Saudi Arabia,” “Iraq,” “Iran,” “Nigeria,” and “Venezuela”) and are subject to being instantaneously shut off (or dramatically reduced) at any point in time. Everybody dips their cups into the reservoir to drink. If any one of those rivers shuts off or diminishes, there is suddenly less water going into the reservoir, and everybody who drinks from it is hurt (the level in the reservoir drops and the price of water spikes upward).

In a global oil market, consumers of oil buy it from wherever it is least expensive. The relative sizes of the above wedges are based on the relative costs of extracting oil and shipping it to the United States.

Imagine a world in which the U.S. produced 15 million bpd domestically, more than meeting our domestic needs, and that we imported no oil from other countries. Now imagine a big supply shock outside the U.S. (a terrorist attack in the Middle East, Nigeria rebels, the Iranian or Venezuelan government shuts off supply just because they can). Those nations that import from the affected country would lose their supply source. They would bid up the price of oil worldwide, including in the U.S. American consumers and firms would have to pay higher prices even though the supply shock occurred in a country from which we import no oil. We are still vulnerable to supply shocks in unfriendly or unstable nations whether or not we import directly from them. We are vulnerable to shocks in the supply of oil, wherever it occurs.

From a rhetorical perspective, we are “addicted to oil” or “dependent on oil.” We are not particularly dependent on foreign oil more than domestic oil. And since it is cheapest to produce oil in the Middle East, to the extent we use oil at all, some of it will always be imported. In terms of the graph above, if a new battery technology were to reduce the amount of oil used in the U.S. by half, and therefore reduce the total area of that pie chart by half, you would roughly expect the pie to shrink There is a counterargument, but it’s a stretch.” You could argue that since foreign oil is a subset of oil, if our goal is to reduce our dependence on oil, it is not inaccurate to highlight a subset of that goal. “Dependence on foreign oil” is not incorrect, a speechwriter or communicator might argue, just misleading. This misleading language, used by the President and Vice President and Members of Congress on both sides of the aisle, creates the impression that this particular problem of foreign oil can be solved. We can reduce our demand for oil in several ways, but we cannot solve the rhetorically attractive but misleading problem if it is defined as “dependence on foreign oil.” Update: A commenter correctly points out that you would not expect the pie to shrink proportionately, but instead for the highest marginal cost producer of oil to drop out first. I believe that is correct as a global matter. It’s harder to tell exactly how dropping the highest marginal cost producer would affect any particular country’s sources, as things would shift around. But my earlier statement about “roughly expecting the pie to shrink” was an incorrect oversimplification. The point that we could not choose which slices to drop still stands.